The foreign exchange markets are the largest and the most liquid compared to any other asset class in the world, primarily due to large volumes pitched in by various market participants- from retail traders to corporates, commercial and investment banks, hedge funds, and other institutions. According to the Bank for International Settlements (BIS) Triennial Central Bank Survey in April 2022, the average daily turnover in the OTC FX markets was $7.5 trillion, up 14% from $6.6 trillion in April 2019.

With so much at stake for investors, let's look at how the forex markets performed in 2023 amid an uncertain macro environment, elevated interest rates, and heightened geopolitical tensions. This will be followed by the outlook for 2024.

Forex markets in 2023

Pandemic restrictions were lifted in early 2023, paving the way for employees to return to work and families to spend time outdoors at restaurants and malls and travel on vacations. However, the global economy continued to be tormented by inflation, partly due to the Russia-Ukraine conflict, driving central banks to extend interest rate hikes to multi-decade highs well into the third quarter despite the threat of a looming recession.

The following were some major themes in 2023 and their impact on currencies.

-

Simmering inflation

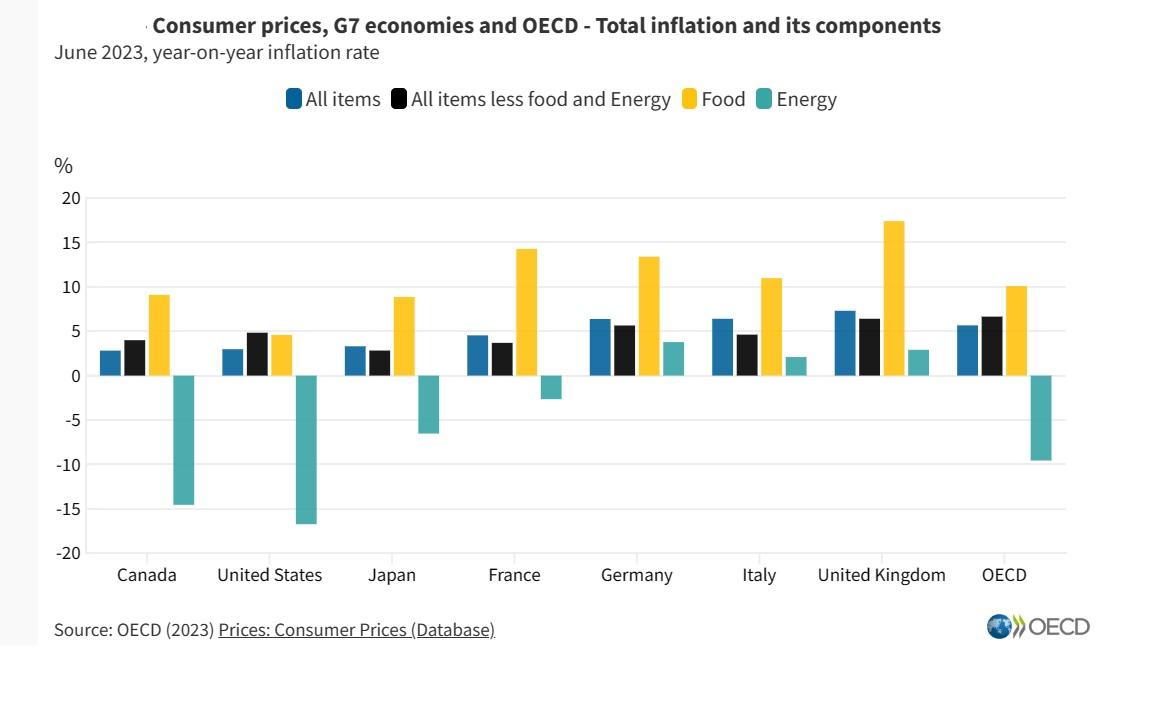

One of the major challenges governments and central bankers worldwide faced was sticky inflation that started during the pandemic and extended into 2023. However, the massive intervention by global central banks to aggressively lift interest rates helped cool inflation from the 2022 peaks, driving the US dollar on the back foot against the other major currencies. While inflation has consistently slid over the past few months, it remains above the target range of most global central banks.

According to the OECD, year-on-year inflation among the OECD countries, as measured by the Consumer Price Index (CPI), declined to 5.7% in June 2023 from 6.5% in May and further as we approached the end of 2023.

As of November, headline consumer inflation in the US and the EU was at 3.1%, while it slid from 4.6% in October to 3.9% in the UK, all indicating that the aggressive rate hikes led to consumers cutting down on purchases, thereby slowing inflation.

-

Pivot in the monetary policy by Central Banks

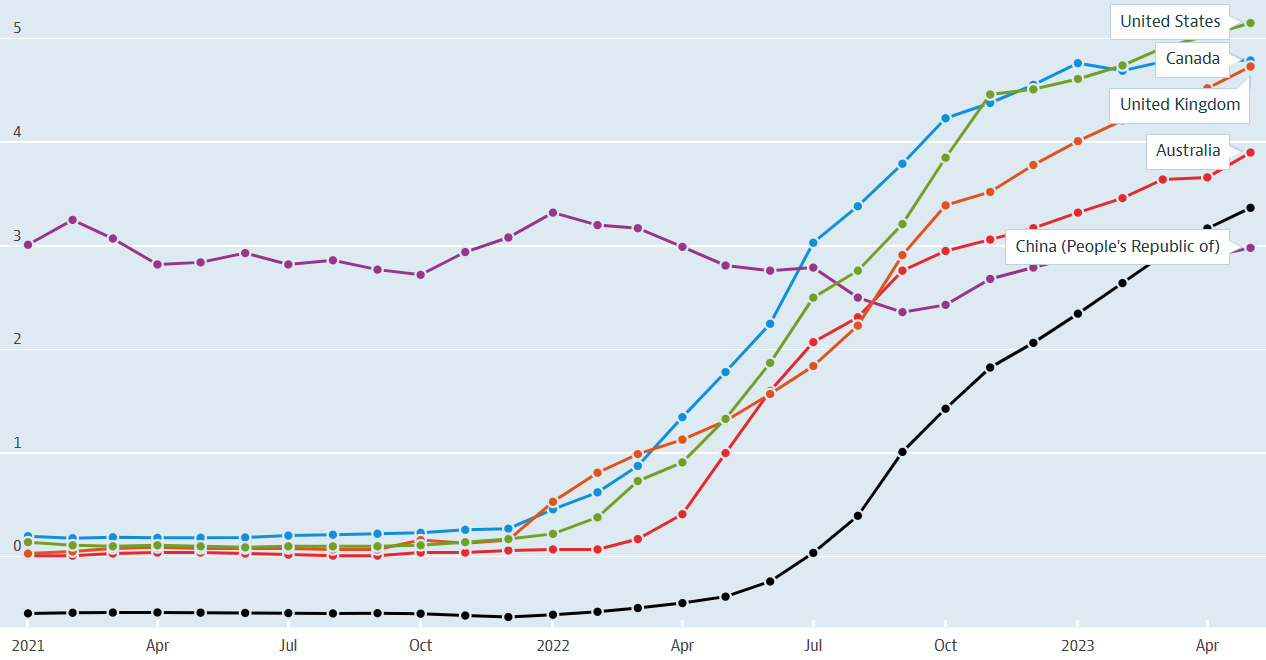

After raising interest rates aggressively in 2022, most global central banks slowed the pace of hikes and even paused in the last quarter of the year amid lower inflation readings and fears of a recession. Some countries like China went the extra mile of easing interest rates and extending stimulus to trigger growth, widening the interest rate differential with most developed economies except for Japan and creating headwinds for the yuan. Meanwhile, Japan's loose monetary policy and the widening interest rate differential with the other developed economies continued to impact the yen, as it succumbed to the third annual drop against the US dollar and the pound sterling and the fourth versus Europe's single currency.

Short-term interest rates

Source: OECD

-

Incorporating ESG factors in forex trading

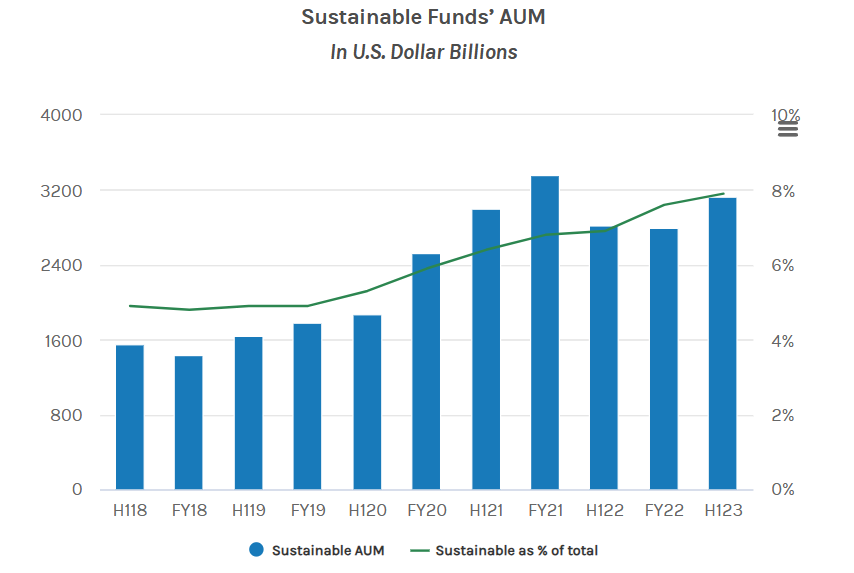

Over the past few years, market participants have also considered the environmental, social, and governance (ESG) framework as one of the criteria for investments. Although investors are yet to contribute to these funds significantly, the AUM of sustainable funds at the end of the first half of 2023 was about $3.2 trillion globally, more than twice since H1, 2018.

Currently, central bank FX reserves such as the Czech National Bank (CNB) are influenced by ESG factors. According to ING, the CNB allocated 3.7% of its forex reserves in the ESG space, while the European Central Bank (ECB) has about 3.5% of its portfolio invested in green funds. The other criteria under consideration are integrating ESG metrics by forex counterparties and banks to offer FX incentives, including lower fees to clients with good ESG ratings. Likewise, market participants could conduct business with banks based on their ESG ratings.

It's probably unclear at the moment how the ESG factor will play a role in the performance of one currency against the other. Based on the current trend, the key beneficiaries are banks, corporations, financial institutions, and others following the ESG framework.

Source: Morgan Stanley Institute for Sustainable Investing analysis of Morningstar data

-

Dollar dominance slows amid geopolitical shift

The US dollar has been the dominant currency for trade and international transactions for decades, but the US currency witnessed considerable de-dollarization for the first time in 2023. Although the dollar maintained transactional dominance, its use in global trade and financial transactions has reduced somewhat. There are several factors, which can broadly be broken down into economic and political reasons.

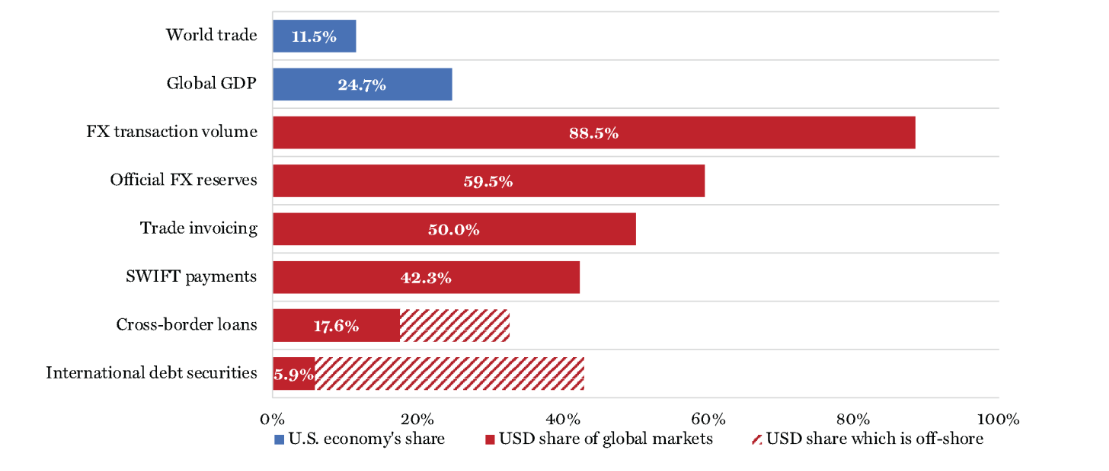

Under economic reasons, analysts believe that while the percentage of US GDP viz-a-viz the world economy has shrunk since World War II and was around 25% in 2022, the transactional volume in US dollars was a staggering 88.5% as of Q2, 2023. In addition, the official FX reserves were 59.5%, with substantial dollar volumes in trade invoicing, SWIFT payments, cross-border loans, and international debt securities, according to BIS. According to analysts, the current dollar-denominated international financial system is skewed in favor of the United States but is unsustainable in the long run.

The political reasons include weaponizing the dollar to promote US foreign policies or punish countries that do not align with US interests, making some countries cautious about being too reliant on the greenback. In 2023, we witnessed substantial bilateral trade in the Chinese yuan, the Russian ruble, and Middle Eastern currencies, such as the Saudi riyal and the UAE dinar. In addition to bilateral trade, the dollar also lost some influence in the energy markets, where considerable sales were transacted in other currencies.

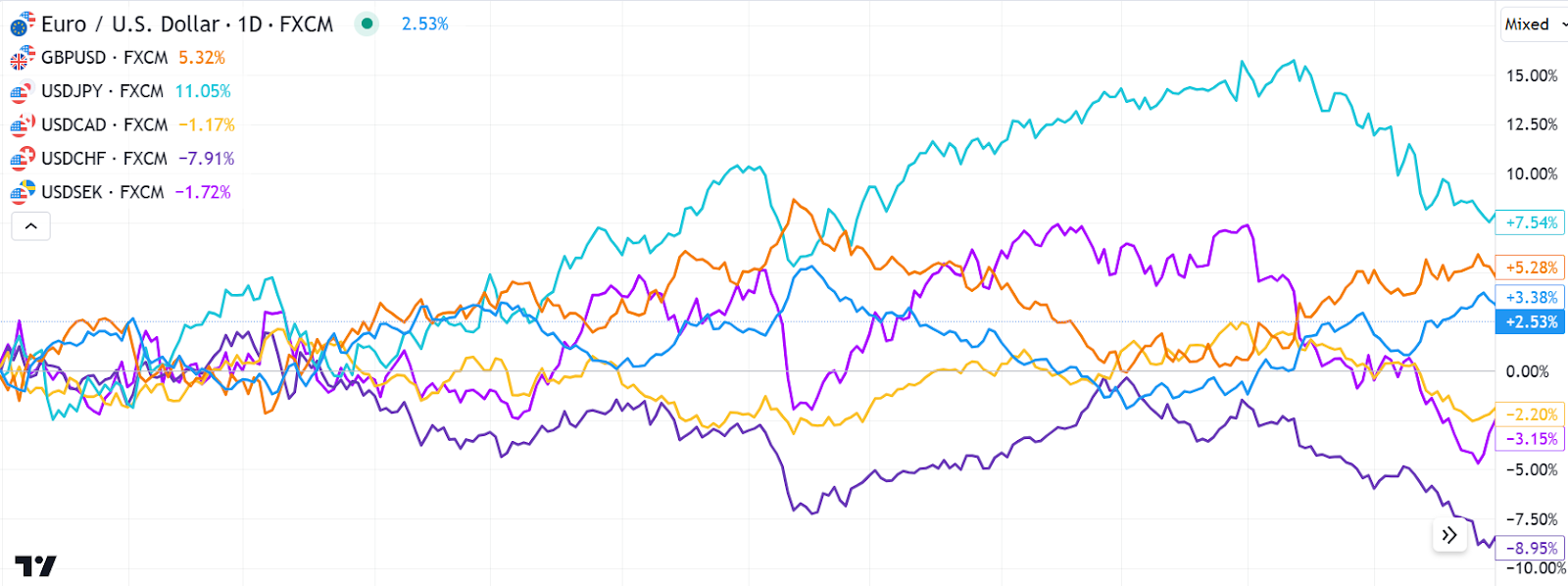

US dollar- Reserves and International Transactions in 2023

Source: internationalbanker.com

To summarize, the US currency, represented by the dollar index (DXY), pulled back last year after peaking at two-decade highs in September 2022. Although the greenback did not come tumbling down, it fell by more than 2.0% against its rivals in the trade-weighted index and has slumped more than 12% from the September 2022 peak.

Performance of the six currencies in the US dollar index in 2023

Forex market outlook for 2024

Most forex pairs were seen oscillating in a tight band in the initial days of 2024, and our outlook of the markets highlights the following critical factors that will drive the performance of individual currencies in 2024.

-

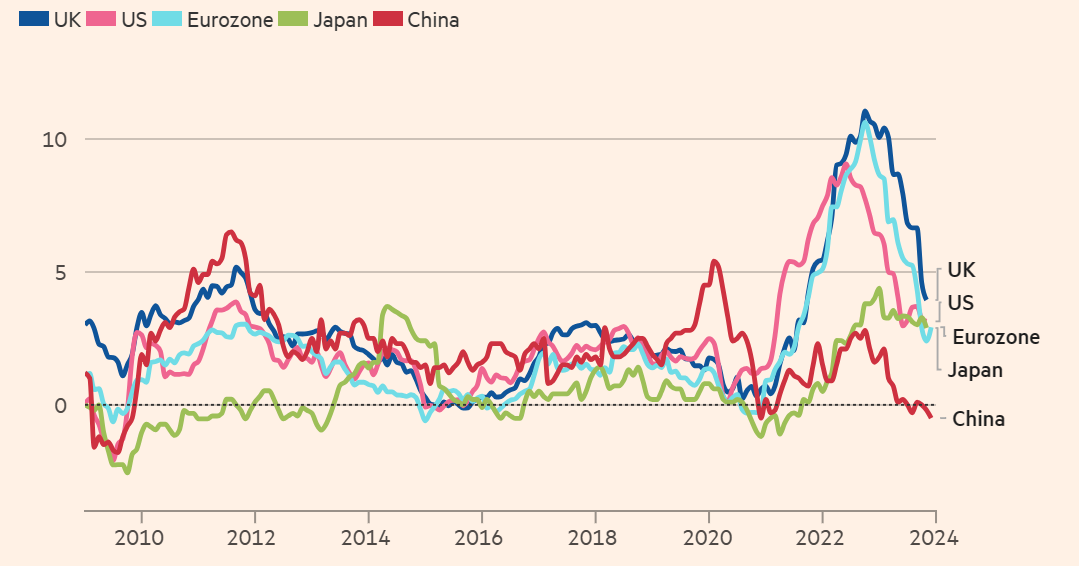

Growth, inflation, and the pace at which central banks cut interest rates

Almost all central banks that raised interest rates aggressively over the past couple of years are expected to pivot to lower rates this year as growth slows and fears of a recession mount. The performance of individual currencies will depend on the pace of economic growth that could impact inflation one way or the other, which central banks will hold on to higher rates for longer, and which ones will blink first.

Among the major economies, analysts expect the European Union to plunge into a recession early this year, while growth in the UK is forecasted to remain weak, meaning interest rates will likely start falling from the first quarter of 2024. The US economy, on the other hand, expanded at an annual rate of 4.9% in the third quarter, primarily from a solid labor market and robust consumer spending. Although traders expect the Fed to cut rates in March, the probability of policymakers holding rates at current levels until May looks more likely.

A poll of economists by Reuters forecasted the US GDP to grow at 1.2% in 2024, even as they are split on whether the aggressive rate hikes by the Federal Reserve in 2022 and 2023 would lead to economic contraction, prompting rate cuts and weakening the US dollar. However, Morgan Stanley does not forecast a recession. Instead, the investment bank expects the Federal Reserve to keep interest rates high into next year.

Meanwhile, Deloitte expects the Bank of Canada to align with the Fed and slash interest rates this year. However, rate cuts will likely happen faster than expected after the Canadian economy shrunk by 1.1% in the third quarter of 2023, the first since the 0.1% annual drop in Q4 2022, while inflation held at 3.1% and the unemployment rate stood at 5.8% in November, both unchanged from the previous month.

Consumer inflation

Source: Refinitiv, FT

-

Geostrategic outlook

The outlook is based on geopolitical events and policy trade-offs, leading to currency volatility. According to Ernst & Young, the current events in Europe and the Middle East have significantly raised the risk of the conflicts escalating this year. In addition, the number of countries heading to the polls in 2024 is the highest it has been in any year in the recent past, elevating the risk of geopolitical surprises. The other geostrategic events are countries racing to innovate and regulate AI, one of the key dynamics in the US-China relationship, navigating a multipolar world, with countries such as India, Turkey, Saudi Arabia, South Africa, and Brazil increasing their foothold in international agenda.

According to JP Morgan, the prospects of the euro rebounding in 2024 are weak as the region is on the brink of a recession as interest rates hover in the restrictive zone after the ECB raised the benchmark refinancing operations rate to multi-decade highs of 4.5%.

The investment bank has a similar outlook for the British pound in 2024. They expect the UK economy to witness sticky inflation, with growth softening. They'd like to see to what extent the Bank of England's monetary policy stance will impact inflation, growth, and the labor market before policymakers pivot to interest rate cuts.

Regarding the Japanese yen, JP Morgan believes structural problems will weigh on the Asian currency this year. However, the bank expects short-term factors like the relative change in the policy rates to drive the currency higher in the second half, although they believe the yen's gains will be light due to the underlying long-run downtrend.

JP Morgan's forecast for the major currency pairs in 2024

Forex forecast for 2024 by other banks/currency analysts

AUD/USD- Bullish outlook with expected target 0.76-0.78 in H1, 2024 from 0.6810 at the end of 2023.

USD/CAD- Bullish forecast of 1.31 by mid-2024, with further upside to 1.42 by November 2024.

GBP/USD- Bearish outlook with a target of 1.11 by mid-2024 from 1.2723 at the end of 2023.

SpainUS

SpainUS