Alpari

Alpari XM

XMAnnual inflation remained above 2.0 percent, underscoring economic resilience

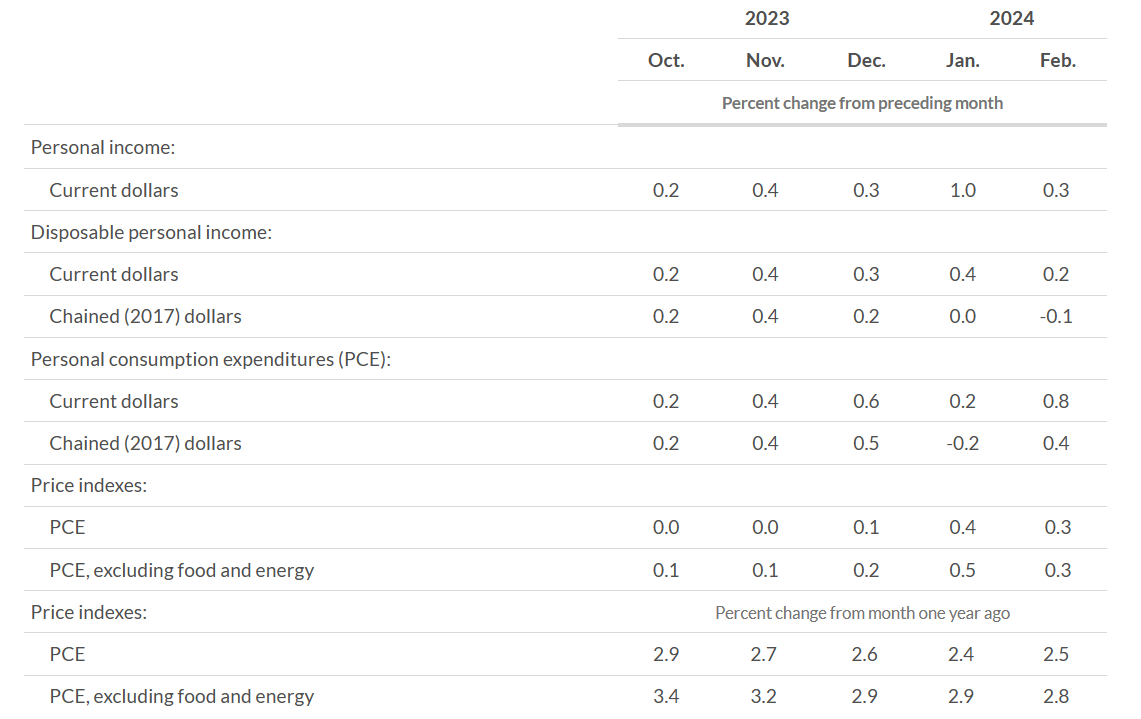

Consumer prices rose 0.3% in February from 0.4% the previous month, and at an annual pace of 2.5% from 2.4% in January as consumer spending rebounded to 13-month highs, the Bureau of Economic Analysis reported on Friday. Meanwhile, core inflation, which excludes the volatile food and energy prices, climbed to 0.3% in February from 0.4% the month earlier and from 2.9% to 2.8% over the past 12 months, the Commerce Department said.

Source: Bureau of Economic Analysis (BEA) website

Consumer inflation is the growth engine of the US economy, and this time around, surging energy costs, a rise in goods inflation, and an uptick in food prices were the key contributors to the PCE price index growth in February. Energy costs jumped by 2.5%, goods inflation rose 0.5%, and the food index registered a 0.1% increase. On the other hand, the cost of services grew by a smaller 0.3%.

The Fed looks at the headline and the core measures but believes the latter is a better gauge to determine long-term inflation pressures, and while the US central bank targets an annual inflation rate of 2.0%, that level has yet to be achieved in the last three years.

The mixed inflation data raised concerns that prices might not trend much lower from here, with some economists worried that Fed policymakers are making a policy error by sticking to the prospects of three rate cuts this year.

In an NPR interview later on Friday, Powell said he was not surprised by the PCE data and believed inflation risks were not elevated. He, however, reiterated that if inflation fails to retract toward the Fed’s target rate or continues higher, policymakers will hold rates at current levels for longer. He also noted that the US economy doesn’t look like it’s in distress from the current interest rate levels.

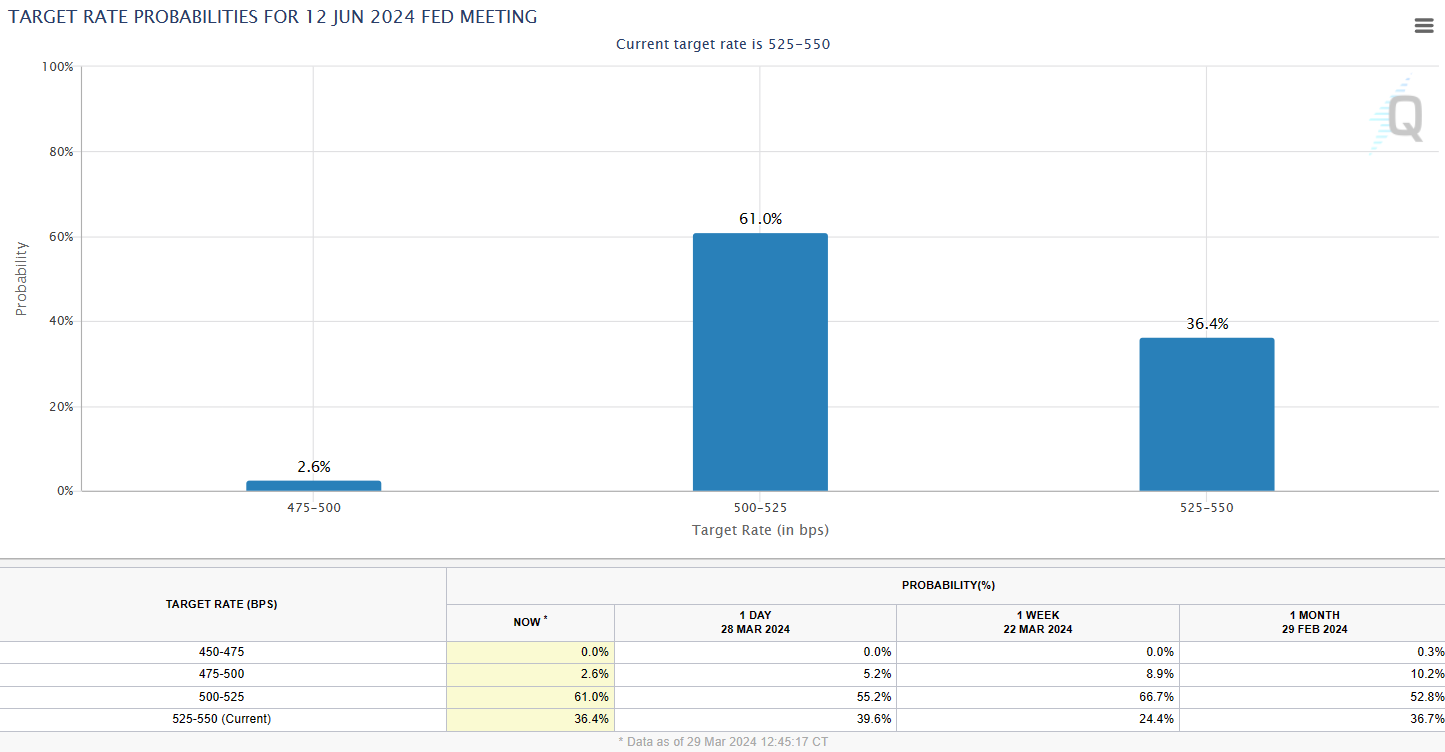

Markets expect the Fed to maintain the status quo on interest rates in May before cutting by 25 basis points at the June 11th-12th meeting. According to the CME FedWatch Tool, following the PCE price index report, about 61% of traders expect Fed officials to lower interest rates in June. That number is up from 55.2% a day earlier and 52.8% a month back.

Source: cmegroup website

Key highlights of the February PCE price index report

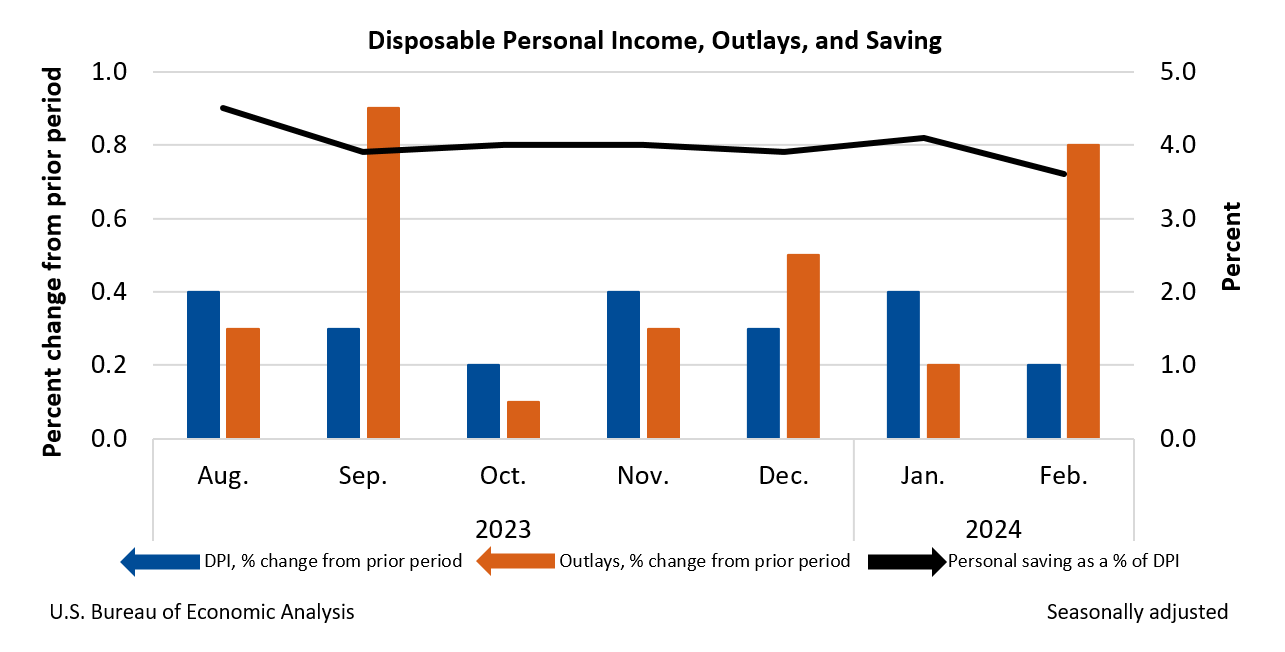

Personal income rose 0.3% or $66.5 billion in February, sharply below the 1.0% growth seen in January and below economists’ expectations of a 0.4% increase. The increase in personal income was primarily from an upsurge in compensation and personal current transfer receipts, which more than offset a drop in the personal income receipts on assets. Meanwhile, disposable personal income (DPI)- i.e., personal income less taxes, rose 0.2% in February, again below the previous month’s figures of 0.4%. On the other hand, real DPI slid 0.1% in February, with inflation in goods up 0.1% and services 0.6%.

The highlight of the PCE price index report was consumer spending, which jumped to a 13-month high of 0.8% in February from 0.2% the month earlier, indicating that consumers still have plenty of buying power despite interest rates at multi-year highs.

The main contributors to the increase in the current dollar PCE in the services sector were financial services and insurance, transportation services, and housing and utilities. In goods, the most significant spending was on motor vehicles and parts.

Market reaction to the personal consumption expenditures (PCE) data

US stock index futures rose for the third consecutive day on Monday after the weaker-than-expected February inflation data reinforced market expectations of rate cuts beginning in June. After a positive opening in the Asian session, the key indices held firm as European markets remained closed on Monday too. The DJIA futures were up 0.30% at 40,296, the S&P 500 futures for June expiry rose 0.37% to 2,328, and the Nasdaq futures traded 0.55% higher at 18,576.

The chief global macro strategist at Ned Davis Research, Joe Kalish, believes the market is fully aligned with the Fed on interest rate expectations, but anticipates increased volatility if inflation fails to dwindle quickly.

US Treasury yields were mixed on Monday, the first trading day of the new quarter, with the rate-sensitive 2-year Note lower by 3.5 basis points at 4.597%, the benchmark 10-year Note down by 0.8 basis points at 4.198%, and the 30-year bond higher by 1.9 basis points at 4.368%. This after the February PCE price index data showed headline and core inflation climb by a smaller 0.3% month-on-month. However, rates on the US government debt registered the biggest quarterly advance in about six months, and while the pullback in yields can be credited to market expectations of a Fed rate cut in June, analysts expect the volatility in the bond markets to continue for the next couple of weeks as investors await key economic releases, such as the March non-farm payroll data and the CPI report.

The greenback was mostly unchanged against its counterparts in the US dollar index on Monday as traders awaited key economic data later this week to drive the benchmark currency one way or the other.

The EURUSD pair hovered near one-month lows, while the Japanese yen oscillated near 34-month troughs against the dollar, with traders monitoring reports from the Bank of Japan closely for signs of an invention. Japan’s central bank last intervened in the currency markets in October 2022 after the yen slumped to 32-year lows of 152.00 against the US dollar.

Technical View

S&P 500 June futures (SPM24)

The benchmark futures settled almost unchanged at fresh all-time highs of 5308.50 on Thursday ahead of the long holiday weekend and before the PCE price index data announcement on Friday. The index faces immediate resistance at 5328, a close above which, the gains could extend to 5390-5400. On the downside, the key near-term support is at 5290. If the benchmark index futures close below this level or break 5260, it could quickly slide to 5140-5160.

Trading strategy:

Go long on the index futures at 5290-5300, with a stop and reverse at 5260 for a profit target of 5390-5400. If the stops are hit, continue holding the short trades with a stop loss at 5320 and exit as the value of the index futures approaches 5160. On the other hand, if the S&P 500 futures continue higher from Thursday’s closing level, go short at 5390-5400, with a stop loss at 5430 for a profit target of 5290-5300. Ensure to trail your profits.

Click the link to view the chart- TradingView — Track All Markets

Synopsis Inc (SNPS)

Synopsis extended losses for the second straight session to close at $571.50 on Thursday, down 0.32%. The stock has fallen close to 10% from the February 26th highs, with the recent rebound failing to extend beyond the previous peak, indicating some weakness in the stock. However, a close above $630.00 will change the view. The near-term trendline support is in the $535.00-$565.00 zone and as long as the stock holds this level, the uptrend is intact.

Trading strategy:

Buy Synopsis at $565.00 with a stop and reverse at $559.00 for a profit target of $610.00. If the stops are hit, continue holding short positions with a BUY STOP at $570.00 and exit as prices approach $535.00.

On the other hand, if the stock extends gains from Thursday’s level, short at $612.00 with a stop at $620.00 for a profit target of $570.00. Ensure to trail profits on the short positions.

Click the link to view the chart- TradingView — Track All Markets